Forum Topics

Reliable, Efficient, and Low-Carbon Resource Portfolios

Setting the Stage for Future Power Market Design

The changing generation mix across the United States is one of the most pressing reasons to modernize electricity markets.

Wholesale energy markets, commonly paired with capacity markets and ancillary services markets, are used to procure the electricity needed to balance the grid and serve load at all times. The observed trajectory of increasing renewable energy development, bolstered by widespread state and local decarbonization goals, point to the need for market structures that better accommodate the attributes of variable renewable energy while maintaining affordable and reliable electricity service.

To better understand what market structures and designs may be needed in a high renewable future, this topic evaluates what types of resources would fit together as part of an efficient, reliable, and low carbon portfolio.

We highlight four studies on this topic, summarized in short slide presentations. These studies show that the United States can reach 80-90% electricity sector decarbonization within the next two decades at little or no increase in cost, with today’s commercially available technology.

The four highlighted reference papers on this topic, and more in the Future Power Markets Forum research library, study options for a low or zero-emission least-cost generation mix.

Mr. Arne Olson of E3, Dr. Jesse D. Jenkins of Princeton University, Dr. Christopher T. M. Clack of Vibrant Clean Energy LLC, Mr. Ric O’Connell of GridLab shared the following slides on the for highlighted papers, to facilitate comparisons. They also offered commentary on the consensus and outstanding questions across the papers.

In summary, the models of a future generation mix show:

- 80+% percent decarbonization is possible with existing technology at modest cost.

- Some amount of “firm” (long duration on-call energy) resources are needed unless there is a massive increase in transmission capacity and responsive demand.

- Multi-day periods without much output from variable renewable resources are the challenge (also known as “dunkelflaute” – German for “dark doldrums”). These periods occur rarely, so the generation needed to serve them will need a compensation scheme that rewards limited generation but long-term availability. The 2035 Report calculated that 100GW will be needed nationally according, operating at very low capacity factors.

- In a deeply decarbonized electricity system, prices are expected to become more volatile but do not necessarily fall on average, depending on the price formation in these instances when variable renewable output is low and power is scarce.

What does a decarbonized future look like?

Diverse examples and studies support the feasibility of operating power grids with high levels of renewables. Many find the that deep decarbonization requires

- Firm flexible zero-emission resources

- Interregional transmission

- Operational and pricing changes in markets.

Market design implications of high penetrations of inverter-based resources

The presentation examines the operational and control challenges introduced by a high share of inverter-based resources (IBRs) such as wind, solar, and batteries in the power system. It outlines the differences between grid-following and grid-forming inverters, emphasizing the need for new market designs and services to ensure system stability and reliability. The presentation also discusses strategies for integrating these resources into the grid, highlighting examples from various system operators and suggesting market adaptations to accommodate the unique characteristics of IBRs.

Relevant Publications

“The Role of Firm Low-Carbon Electricity Resources in Deep Decarbonization of Power Generation”

Nestor A. Sepulveda, Jesse D. Jenkins, Fernando J. de Sisternes, Richard K. Lester

Published in Joule, Volume 2, Issue 11, 21 November 2018, Pages 2403-2420

“Pacific Northwest Low Carbon Scenario Analysis: Achieving Least-Cost Carbon Emissions Reductions in the Electricity Sector”

Arne Olson, Nick Schlag, Jasmine Ouyang, Kush Patel, Oluwafemi (Femi) Sawyerr, December 2017

“Minnesota’s Smarter Grid”

Vibrant Clean Energy LLC, July 2018

2035 Report

Goldman School of Public Policy, June 2020

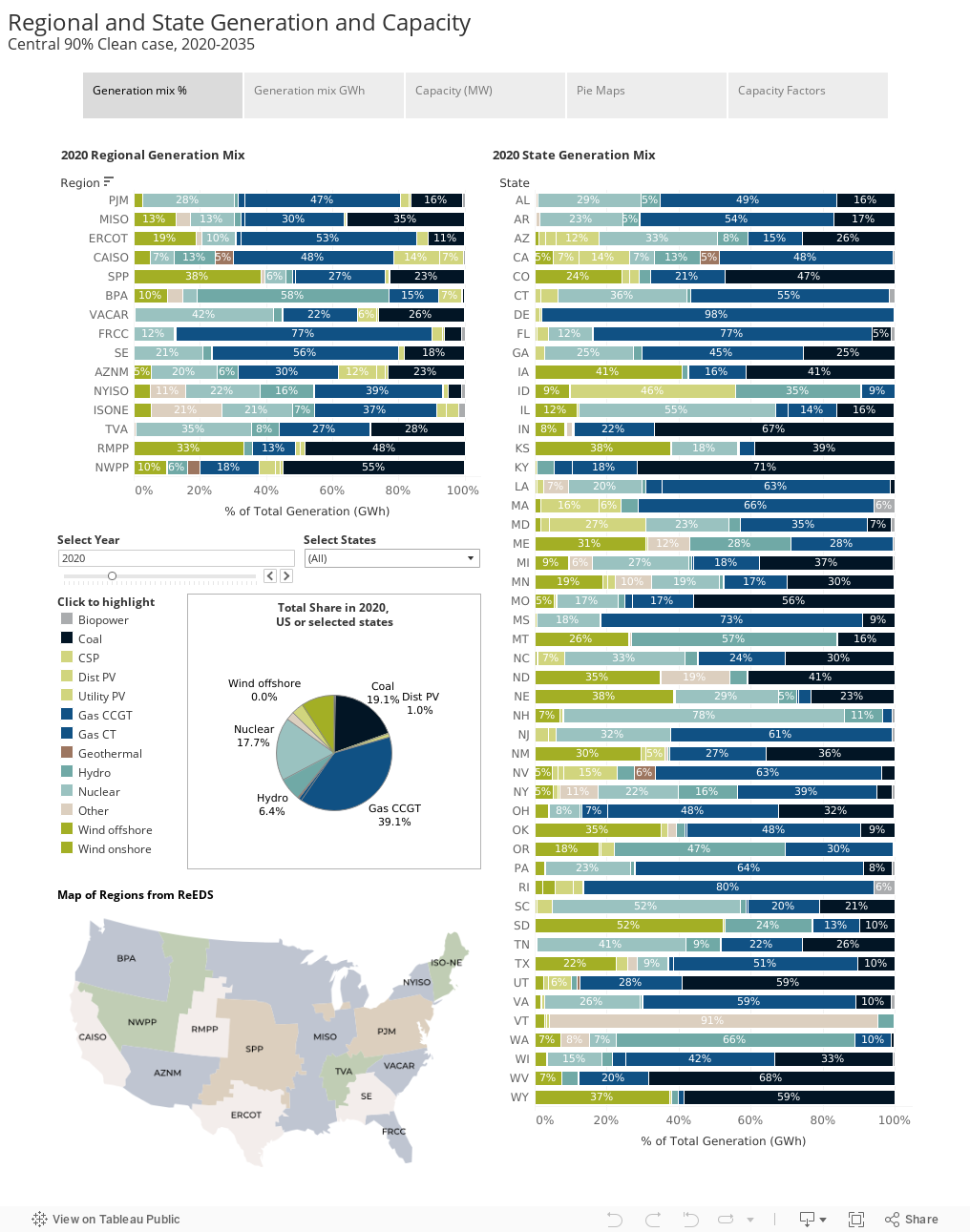

2035 Report Resource Mix Model for 90% Decarbonization

The interactive visualization below, created by Bentham Paulos, demonstrates the shift in resource mix across the United States since 2010, and uses the 2035 Report model to project a technically and economically feasible path to 90% clean generation by 2035.

Expert Commentary

These comments are personal opinions and do not represent the official position of an expert’s employer or clients or the Future Power Markets Forum.

Mark Dyson, Rocky Mountain Institute

It is encouraging that there is an emerging consensus among leading analysts around the shape of least-cost, near-zero carbon resource portfolios that can also support economy-wide decarbonization through electrification. In particular, even though analysts may disagree on the specifics of long-run decarbonization, there is a clear consensus among leading modeling studies around the first steps: near-term expansion in wind and solar and planning for significantly increased transmission and electricity demand are least-regrets options for every region of the country, providing both a foundation for least-cost decarbonization as well as near-term economic value.

Travis Fisher, Electricity Consumers Resource Council

The Future Power Markets Forum is already asking the right questions. I’ll add one more: how can we do an honest assessment of the all-in cost of delivered electricity? Too often we hear about the falling levelized cost of energy (LCOE) or very low power purchase agreement (PPA) prices, but from a societal perspective (one that I’d like policymakers to embrace), those are not the whole picture. The typical consumer doesn’t care about a record-low PPA. Further, the growth in generation that (1) is intermittent and (2) requires new transmission to be built increasingly makes stand-alone LCOE a bad metric. I think if we could model the all-in cost of electricity more effectively, we could make better policy decisions. For example, we could more definitively answer questions about the cost of shutting down or retaining existing generation resources (thinking especially about large, low-carbon facilities like existing nuclear plants). We could also understand the full implications of resource portfolio targets and mandates.

Rana Mukerji, New York Independent System Operator

The NYISO study results on the transition to a clean and sustainable grid in support of the New York in support of New York’s Climate Leadership and Community Protection Act (CLCPA) are largely consistent with observations of Messrs. Olson and Jenkins.

The transition from today’s grid to the 2040 system will see a shift away from emitting generators (primarily fueled by natural gas) and towards zero emissions wind and solar resources. Loads will also grow as other sectors of the economy electrify. A few key factors drive the composition of potential resource mixes including the need for flexible resources and the availability of transmission from upstate to the downstate load centers.

Many existing fossil fuel plants can be dispatched to a rated output level for extended periods, while also offering a level of flexibility to ramp up or down as needed to continuously balance load and supply. To the extent that the CLCPA leads to the elimination of all fossil fuel-based resources supplying the grid, the carbon-free resources supplying the grid will need to offer comparable flexible capabilities, individually or collectively.

Batteries and load flexibility can provide short-term balancing to address hourly balancing challenges, but the ability of these resources to be a longer-term reliable resource depends on a battery’s ability to charge and then provide enough MWh as needed; and for demand response’s ability to respond quickly and perform for sustained periods. To provide a dispatchable, sustained response over multiple days or seasons is a much more difficult challenge requiring new technologies such as carbon sequestration, renewable natural gas or large scale flow batteries. All NYISO studies examining higher penetration of renewable resources have identified the need for flexible, dispatchable, emission-free resources to reliably operate the grid and satisfy the CLCPA.

These flexible supply technologies address the multi-day and seasonal balancing challenge and might include long-term storage, renewable natural gas, hydrogen, more price-responsive load, and/or flexible imports. In all likelihood, achievement of the requirements of the CLCPA, while maintaining reliability, will require a combination of these approaches to match supply with demand. It is too soon to know with certainty what technologies will be available, but the NYISO will continue to prioritize developing market enhancements to incent innovation and investment in resources with the needed flexible capability.

It is to be noted that it is theoretically possible to achieve the CLCPA Goals without new technologies like renewable natural gas through more flexibility from expanded interties (particularly with Hydro Quebec) and more flexible load (primarily from electric vehicles and flexible HVAC systems) and installing significantly more in capacity wind and solar and conventional storage resources. However capital costs of such a system as well limitations on sites make this an unlikely outcome. Future innovations on new technologies for a clean dispatchable resource capable of providing a sustained response over multiple days a more viable path to reach the zero carbon goal that the New York CLCP envisions.

Andrew Ott, Formerly PJM Interconnection

From a system operations and sustainability perspective the overall findings stated by the presenters made intuitive sense. The presenters agreed that in order to achieve low or zero carbon emissions in the power sector, at least one form of Firm low carbon resource is necessary. From a system operations point of view, I would agree and further suggest it is necessary to have several forms of Firm low carbon resources to achieve sufficient supply diversity to ensure stable and reliable operations under all conditions especially extreme weather conditions.

From the presentations, it is obvious that developing some combination of storage technology and other alternative, distributed technologies to enable demand flexibility will be a key to achieving emission reduction targets in a reliable and least cost manner. It makes sense that these technologies can be leveraged to offset intermittent resource inflexibility and help increase the amount of renewable resources that can be incorporated into the grid. It seems a great opportunity to reduce the overall cost of the energy transition. However since many of these storage and advanced technology resources are smaller and distributed, it seems necessary to evolve the regulatory processes and market designs to promote and incent these resources in order to achieve the necessary scale. Also seems that much better wholesale / retail coordination will be necessary which could be a challenge in the current regulatory environment.

Karen Palmer, Resources for the Future

To varying degrees, these presentations on resource portfolios recognize a growing role for flexible electricity demand in facilitating the integration of variable resources and helping to support the value of incremental renewables. Demand flexibility will depend on incentives associated with electricity rate design or service pricing, ease of demand scheduling or price responsiveness for electricity consumers of various types and receptiveness of consumers to surrendering control over devices to the utility or a third party, among other factors. What are the key policy and technical barriers to greater demand side engagement in electricity markets? What are the most important research questions that need to be addressed to move flexible demand to the next level?

Michael Panfil, Formerly with the Clean Energy Buyers Association

The power sector exists to meet the needs of its customers. And customers are increasingly unified in what they want: a system equipped to integrate clean technology and innovation, built on zero-carbon generation, and operated at lowest-cost. Achieving this outcome will require thoughtfully constructed and well-implemented market design. Although robust debate exists as to the precise elements requisite to that market of the future, there are encouraging signs of agreement on fundamentals. There is no question, for example, that a zero-carbon system can deliver reliable, cost-effective electric service. Nor is there substantial disagreement among customers that competitive wholesale markets are best-suited to accomplishing flexible, equitable, least-cost power sector decarbonization. Most likewise agree that market design turns on improving implementation to achieve promised benefits. This customer-centric focus and these foundational points of consensus should guide debate and iteration around the future of market design.

Charlie Smith, Energy Systems Integration Group (ESIG)

The topic of resource portfolios and the changing resource mix brings up the question of how we will measure resource adequacy (RA) methods in the future. In the past, we only considered generation in the equation. In the future, we will need to consider variable energy resources, energy storage, electric vehicles, flexible load, and demand response. Our RA methods need to evolve along with our resource mix to enable markets to provide what consumers desire.

Power Market Structure and Design

If you have something you would like to contribute to the topic you can include your comment here.